The world of finance has experienced a profound transformation in recent years, driven by advancements in technology. Among the most notable shifts is the way lending processes have evolved. Gone are the days of filling out lengthy paper forms in a bank’s office, waiting weeks for approval, and wondering whether or not your creditworthiness will pass muster. Thanks to modern technologies in lending, the process has become more efficient, transparent, and accessible than ever before.

One of the most significant developments in this transformation is the rise of online applications. Coupled with the advancement of credit scoring systems, this shift has fundamentally changed the way individuals and businesses obtain loans. In this article, we will explore how online lending applications and modern credit scoring technologies are reshaping the lending landscape.

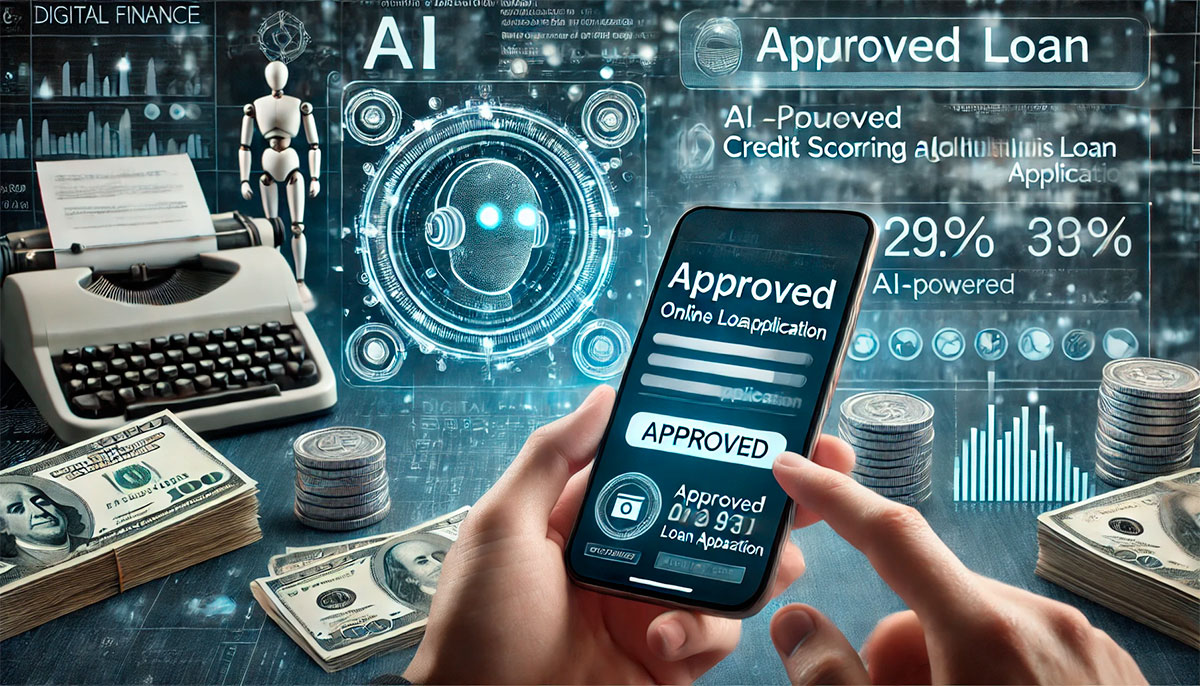

The Rise of Online Lending Applications

In the past, securing a loan often involved hours of paperwork, phone calls, and personal meetings with a bank officer. For many, this process was not only tedious but also an obstacle to obtaining the funds they needed. With the advent of online lending platforms, however, this traditional method has become almost obsolete.

Today, borrowers can apply for a loan from the comfort of their own home, at any time of day, using only an internet connection and a device. The online application process is streamlined, allowing individuals to apply for everything from personal loans to mortgages with just a few clicks. Platforms such as peer-to-peer lending websites, fintech startups, and even established banks have embraced this technology, making it easier than ever to access credit.

One of the key benefits of online lending applications is the speed at which borrowers can receive a decision. Traditional banks often take days or even weeks to process a loan application, while online lenders can provide approval within minutes, if not instantly. This rapid response time is possible because these platforms rely on automated systems to assess applications, which leads to quicker decision-making.

Moreover, online lending applications have made the process more inclusive. Borrowers from various backgrounds and locations can apply for loans, even in cases where they might not have had access to traditional banking services. Rural residents, people with non-traditional employment histories, or those without a significant credit history can now apply for loans without leaving their homes, all thanks to the convenience and reach of online platforms.

The Evolution of Credit Scoring

As online applications revolutionized the way loans are accessed, another crucial aspect of modern lending has also undergone a significant transformation: credit scoring. In traditional banking, credit scores have been the primary tool for assessing an individual’s or a company’s creditworthiness. However, the methods used to calculate these scores have not always been transparent or inclusive.

Historically, credit scoring models such as FICO (Fair Isaac Corporation) were based on a variety of financial factors, including payment history, debt levels, and the types of credit used. While this system was effective for many borrowers, it also had its limitations. For example, individuals who had never used credit before (such as young people or recent immigrants) might not have had a credit score at all, making it difficult for them to secure loans. Additionally, people with lower credit scores were often penalized by the system, even if they had other financial assets or a steady income.

In response to these challenges, modern credit scoring systems have begun to evolve. Today, more innovative and comprehensive models are being employed, which take into account a broader range of factors beyond just credit history. For instance, alternative data sources, such as utility bills, rental payments, and even social media activity, are being used to help create a more complete picture of a borrower’s financial behavior.

Machine learning and artificial intelligence (AI) have also made their mark in the credit scoring space. These technologies can analyze vast amounts of data and identify patterns that traditional credit scoring systems might miss. AI-powered credit scoring models can consider variables such as job stability, education level, and other non-financial indicators to more accurately assess an individual’s ability to repay a loan. These advancements have not only improved the accuracy of credit assessments but have also made it possible for lenders to approve a wider range of applicants.

In addition to benefiting borrowers, modern credit scoring technologies have also enabled lenders to reduce their risks. By using more sophisticated algorithms, lenders can more precisely predict the likelihood of a borrower defaulting on a loan. This leads to lower default rates, better risk management, and ultimately, more profitable lending practices.

The Role of Big Data and Artificial Intelligence in Lending

At the heart of many modern lending platforms is the use of big data. In the past, lending decisions were often based on a limited set of factors—primarily credit scores and financial statements. However, the advent of big data analytics has allowed lenders to gain deeper insights into borrower behavior and financial habits, enabling them to make more informed decisions.

Big data refers to the large volumes of information generated by individuals, businesses, and institutions every day. This data can include everything from purchasing habits and transaction history to social media interactions and location data. By analyzing this data, lenders can gain a better understanding of a borrower’s overall financial situation, even in cases where traditional credit scores may not be available or sufficient.

Artificial intelligence plays a pivotal role in this process by analyzing and interpreting the vast amounts of data at a scale that would be impossible for human analysts. AI-powered systems can identify patterns and correlations that would otherwise go unnoticed, providing a more accurate picture of a borrower’s likelihood of repayment. Moreover, these systems can continually learn and improve over time, making lending decisions increasingly precise.

The combination of big data and AI not only improves the accuracy of lending decisions but also enhances the customer experience. Borrowers can receive personalized loan offers that are tailored to their specific financial profile, rather than being subjected to one-size-fits-all lending criteria. This personalization leads to more favorable outcomes for both borrowers and lenders, as loans are better matched to an individual’s ability to repay.

The Future of Lending: More Accessible and Efficient Than Ever

Looking ahead, it is clear that modern technologies in lending—especially online applications and advanced credit scoring systems—will continue to shape the future of finance. As technology advances, the lending process will become even faster, more efficient, and more accessible to people around the world.

One of the most exciting developments on the horizon is the potential for blockchain technology to further disrupt the lending industry. Blockchain could provide a secure and transparent way for borrowers and lenders to interact, reducing the need for intermediaries and lowering the cost of lending. Additionally, blockchain’s ability to provide tamper-proof records could enhance the security of credit scoring systems and reduce fraud.

As the lending industry becomes more data-driven, it is also likely that we will see an increased focus on financial inclusion. With improved access to credit for underserved communities and individuals, more people will be able to access the capital they need to grow their businesses, invest in education, or simply improve their quality of life.

In conclusion, modern technologies in lending—online applications and advanced credit scoring systems—have fundamentally transformed the financial landscape. By making lending faster, more inclusive, and more personalized, these innovations have opened up new opportunities for both borrowers and lenders. As technology continues to evolve, the lending process will only become more efficient, providing greater financial access to people all over the world. The future of lending is here, and it is more accessible than ever before.